The burden of proof lies with proof of the burden

Just another migration here—this piece questioning the idea that dollar centrality constitutes an exorbitant burden on the US economy was first posted on Medium in April 2023. I thought this belonged on the stack as well because, among other things, this lays out another element of my skepticism regarding some of the dominant narratives in a certain strand of US political economy discourse . So it can be read in conjunction with this and with this. Here it is.

At his semi-annual congressional testimony in early March, Fed Chair Jay Powell was asked by Ohio Senator J.D. Vance (J.D.) if the role of the dollar as the global reserve currency had “some downsides and not just upsides.” Vance, being Vance, was unable to resist adding that “When I look at the American economy, we have a lot of financial engineers and a lot of diversity consultants. We don’t have a lot of people making things. And I worry that the reserve currency status, and the lack of control we have over our currency, is perhaps driving that.”

Powell mostly dodged the question, observing “Now, so, of course, we benefit by being able to pay for our goods all over the world, pay for everything, anywhere in the world, mostly, with dollars. That is an advantage. You know, there are some economic theories around it that it also has burdens of various kinds. But I can’t call it all back to mind.” He also noted that the dollar had no real competitors right now and punted the issue of the dollar’s valuation to the US Treasury. This, of course, was particularly coy, since the Fed has become much more willing to opine about the dollar in recent years — an evolution that I am particularly delighted to see. https://www.tumblr.com/rajakorman/114124758065/the-fed-never-talks-about-the-dollar-and-other.

But the Senator for Ohio is not alone in asking this question. In recent years, there has been a string of blogs, opinion pieces and articles laying out the case that the centrality of the dollar in the global financial system has led to excessive currency strength that has disfigured the US economy, accelerated US deindustrialization, and strengthened an anti-globalization backlash that led to the election of Donald Trump, and altered (perhaps permanently) the ideological and sociological make-up of the Republican Party. This is most often expressed as the belief that rather than an Exorbitant Privilege, dollar centrality is an Exorbitant Burden for the United States — a view found here https://carnegieendowment.org/chinafinancialmarkets/56856 and here https://www.phenomenalworld.org/analysis/the-class-politics-of-the-dollar-system/

But, as the title of this piece of suggests, I disagree with this idea (which means I disagree with many friends). While I think are are problems that stem for the US from the centrality of the dollar in global finance, I also think that a) dollar centrality (a feature of the entire post-1945 era) is not always associated with dollar strength after the transition to floating exchange rates in 1971 b) there are periods of dollar strength that stem from factors other than its centrality c) compared to just about every other country in the world, the US gains in aggregate more than it loses from dollar centrality d) the burdens of dollar strength are regionally and sectorally concentrated, but these could be alleviated (and yet have not been) by the benefits of low (lower than otherwise) interest rates that flow from a demand from dollar assets e) the US is sufficiently heterogenous in terms of resource endowments and the technological sophistication of different industries that there is never going to be a single level of the dollar that is right for all sectors f) while trading desks are full of people who tend to think of exchange rates as stock prices who respond to dollar strength with a combination of jingoism and satisfaction when they’re long, Wall Street as a whole has a smaller role in global dollar intermediation than banks in Europe, Japan, Australia and Canada. Meanwhile, institutional finance in the US is largely indifferent to what the dollar is doing as long as its moving in a way that flatters profits, valuations, and prints more transaction tickets g) While the economic benefits of dollar centrality are overstated, and so — to an even greater degree — are its costs, the gains from using of dollar centrality as a tool of global political suasion are substantial AND jealously guarded by the US security and diplomatic establishments.

The Dollar of the International Monetary System and The Market Dollar

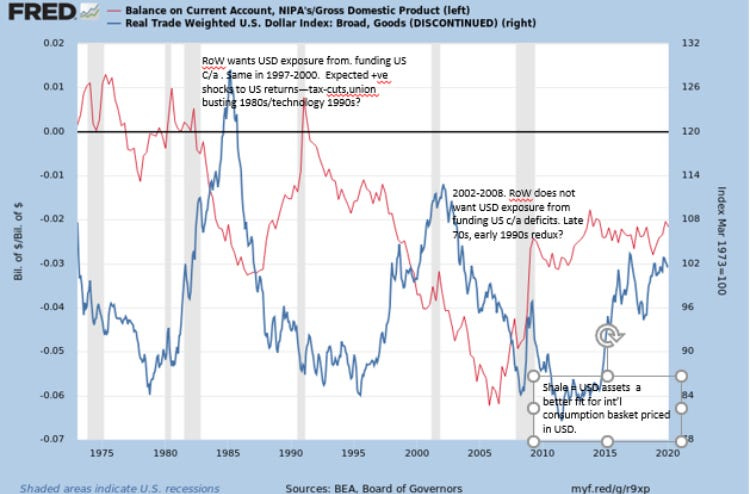

On to the substance in a bit more detail. One of the claims of “burdeneers” (to coin a word) is that the world’s demand for dollar-denominated assets leads to persistent currency strength that has penalized the US tradable sector, particularly manufacturing. But the dollar has had pretty tumultuous ride in foreign exchange markets since the end of the Bretton Woods era in 1971. Large current account deficits (the obverse of a putative increased demand for dollar assets) have coincided with both a stronger dollar (most obviously in 1981–85) and with a weakening dollar (as was the case during much of the 1970s, and between 2002 and 2008). I have written about this at greater length here — https://medium.com/@karthiksankaran/the-market-dollar-the-imfs-dollar-7d9feebbfdd — but the simple point is that long-stretches of dollar strength are typically the result of an increased appetite for US assets driven by the belief of investors in the rest of the world that the US has experienced a positive technological, policy-driven rate-of-return, or terms of trade shock. Conversely, when none of these positive features are present, growing US current deficits remain “funded” but the desire of private investors in the rest of the world to hold the dollars they receive in payment falls, and with it so does the currency. The chart below is from the above piece in Medium — I use it because the Fed’s reworked trade-weighted dollar index (the old index has been discontinued) only goes back to 2006.

Just Regular Dutch Disease

The most recent portion of the graph also shows the dollar rally that began in 2014 and continued (at least) into late 2022. This is worth singling out because it captures the dramatic shift in the US’s balance-of-payments dynamics that resulted from the shale revolution. As pretty much everyone knows by now, the US went from being the world’s largest oil importer to being an energy exporter inside a decade. The important point here is not so much that the US current account deficit shrank dramatically — at 3.4% of GDP it is wider than it was in 1985, but it is still substantially smaller than the wides around 6.3% of GDP in late 2006. It is rather that shale has given the dollar the attributes of a commodity currency — an asset that appreciates when commodity prices rise, rather than depreciating, which was how the dollar behaved in the 1970s and early 2000s. This matters because the import basket of much of the rest of the world contains a lot of energy, and a world where energy prices are rising but the dollar is falling is one where the US currency becomes a hot potato that no-one wants to hold — as happened 2006–08. This suggests that the US after 2014 might just have regular Dutch Disease to a greater degree than any exotic financial variant of the same. However, I will concede (and this is a point I have taken from conversations with Brad Setser) that dollar strength versus the euro and the yen in the years after 2014 (when both currencies had positive terms of trade shocks resulting from the shale-induced fall in global prices) was exacerbated by the Eurozone’s single-minded focus on a monetary (and by implication exchange-rate) tool, rather than on fiscal policy, to exit the crisis. Abenomics in Japan also worked in similar ways. Still, this do not seem to me to be a “centrality” argument per se.

If you hate being able to print dollars, try owing them without having any

The term Exorbitant Privilege was coined by Valery Giscard d’Estaing when he was France’s finance minister in the 1960s, but he was drawing on the thought of Jacques Rueff who wrote that the centrality of the dollar (and its substitutability for gold) under the gold-exchange standard that prevailed between 1945 and 1971 allowed it to run “deficits without tears.” And it is indeed true that the ability to settle external liabilities in a currency that one’s central bank can produce at will erases the threat of sudden stops, balance of payments crises, dramatic shock-therapy adjustments imposed as a condition for external financing, etc. And when that currency is the dominant currency in the international system, it gives the ability to do all those things to another country, but more about that later. For the moment, it at least suggests some of the pitfalls that the world’s largest external debtor is able to avoid compared to many smaller debtor countries. It is fair to retort that those things only happen to developing countries and not to developed ones like Australia, Canada, or the UK.

But even here, the US has certain advantages. The dollar’s centrality as the dominant currency for invoicing international trade means dollar weakness is much less likely to feed into domestic inflation in the US — more than 90 percent of US imports are priced in dollars, far higher than any other country. The low passthrough into inflation is both a function of inertia in pricing and the fact that the sheer size of the US economy makes importers more likely to absorb reduced profitability in their margins rather than run the risk of losing market share. One thing to note here is that low inflation passthrough also allows a larger portion of nominal depreciation to “stick” as real depreciation. Gita Gopinath, currency first deputy MD of the IMF has written extensively on the subject, including here https://www.kansascityfed.org/documents/5753/2015-jackson-hole-gopinath-the-intl-price-system.pdf.

Conversely, the centrality of the dollar in global invoicing and its role as the dominant currency for cross-border borrowing (particularly in emerging markets) mean that dollar strength can push inflation higher outside the US — particularly when this occurs alongside negative commodity supply shocks, as experienced in 2022 — as well as raise the burden of debt for dollar borrowers. Episodes of dollar strength may suck for the US, but they suck even more for current-account deficit emerging markets (and even the occasional developed market like Australia and Canada in the late 1990s) bounced into cyclically unnecessary rate hikes. It is possible then that any impacts of dollar strength on US export performance reflect not only a loss of exchange-rate competitiveness, but also (and perhaps more importantly) a tightening of global financial conditions that pulls down world aggregate demand.

Is the USA an OCA?

This is not to deny that dollar strength does not have costs within the US. However, as noted above, I remain unconvinced that dollar centrality is always associated with dollar strength and that recent dollar strength is solely the result of centrality — or as phrased above, it reflects conventional rather than financial Dutch disease. But even within the US, I would argue that the costs of dollar strength are localized; may be insurmountable to certain extent; and susceptible to better remedies that have not been sufficiently utilized.

In my view, the problem is less that the exchange rate is too strong for the entirety of the US industrial plant but rather that sheer size means the US contains remarkably heterogenous technological capabilities among industries with very different susceptibilities to catchup growth in the rest of the world. I have tended to think about this as the economic fortunes of regions in this century being captured by a simple rubric — does this region make what China (or increasingly — broader East and South Asia) needs/wants or what China makes? This rubric is something people find intuitively obvious about the Eurozone when they ask — does it make sense for Germany and Portugal to share a currency? But the same question applies to say North Carolina and California or Washington. In other words, any sufficiently large internally heterogenous currency and customs area composed of sectors both at or near the technological frontier (say Boeing or Microsoft) and those very distant from it (furniture manufacturers) will find it difficult to get the exchange-rate “right” across sectors. Further, even in the absence of reserve accumulation (whether prudential or mercantilist), if such an economy has an open capital account, it will likely experience inflows of capital seeking to gain exposure (or ownership) of the most productive and technologically-advanced sectors.

There is also a common argument that demand-suppression in Asian emerging markets as part of a mercantilist strategy reduces their capacity to import American goods. I have some sympathy for EM efforts to avoid crippling balance of payments crises, but even conceding this point, it seems unlikely to me that any increase in EM imports of US goods would benefit the US regions that have been most susceptible to EM catch-up growth. To return to the regional dichotomies used above, richer EM consumers might take more trips on Boeings but they are unlikely to buy more furniture made in North Carolina. The issues of concentrated regional plant that is exposed to rapid economic advances outside the US might be better dealt with by something the country undoubtedly enjoys.

An Exorbitant Privilege In Interest Rates?

I also think that to the extent that there is a persistent inflow into US (putatively) safe assets, such as Treasuries and Agency MBS, there is likely an effect on US interest rates. This is not just a result of flows, but also a result of the Fed’s reaction function to dollar strength. Thanks to a welcome bit of perestroika that followed Stanley Fischer’s tenure as Deputy Chair, we now know that the Fed thinks about the dollar a lot, sees dollar strength as tightening both US and global financial conditions, and is willing to put numbers on it. In September 2016, Lael Brainard told us that a 20 percent move in the dollar has roughly the same impact as a 2 percent move in interest rates — known in the jargon as a 10 to 1 MCI. https://www.federalreserve.gov/newsevents/speech/brainard20160912a.htm.It is probably worth noting that the equivalent for the Eurozone is 6 to 1 (per the Commission’s Directorate General of the Economy), and the Bank of Canada used to operate on the basis of a 3 to 1 MCI. This gives some indication of how closed the US economy is, in turn suggesting how exorbitant (or not) the burden is.

Another way to think about this is that the exchange rate effects of dollar centrality may be a burden for a very small portion of the US workforce, while the interest rate effects (i.e., lower interest rates that result from global demand for safe US assets) have the potential to be a windfall for a much larger portion of the US workforce. This is because the US is fundamentally a more interest-rate sensitive economy than it is an exchange-rate sensitive economy. And this suggests that there enormous possibilities to do useful things with such “cheap” financing — push further out the technological frontier, build better infrastructure, finance transitions for workers affected by globalization and/or technological change. There are certainly lots of problems in immense US non-tradable sectors that affect a larger number of people than are affected by periods of excessive dollar strength.

Why then has this interest-rate windfall often been squandered? I would suggest that this is because of an artifact of the 1980s and 1990s that I remember (because I used to spout it). This is the hypothesis that “twin deficits” are particularly problematic because they reflect governments engaging in “unsustainable” borrowing from foreigners to do stupid things with the money — because that’s what governments do with borrowed money compared with households and businesses who borrow wisely. Luckily, we may be at a long-overdue point in US political economy where that conventional wisdom is being challenged.

Finance Less Proud, Industry More Content?

Similarly, I think there is little to substantiate the widespread narrative that US financial institutions are in particular interested in dollar strength as a means to protect their position in global finance. That overlays on the current system a model from the era of the classical gold standard, where British finance insisted on (and secured in 1925) a return of sterling to the gold standard at its pre-war parity. Churchill was Chancellor of the Exchequer at the time and succumbed to the pressure — despite almost being persuaded otherwise by Keynes — and having once said he would rather see finance less proud and industry more content.

However, I view this analogy as fundamentally misplaced. First of all, foreign financial institutions play a bigger role in intermediating dollars globally than does the US financial system — Banks outside the US have about three times the cross-border USD claims of US banks (a combination that frequently has them tumbling over their skis). See the chart below from the BIS. Further, despite the terminology of “global reserve currency” I believe that dollar centrality depends not just on its value as an asset — but also (and perhaps even more) on its use as the dominant currency denomination for cross-border liabilities. And the financial role of the dollar as the world’s central currency has likely been amplified during “weak dollar” moments, when there are lots of dollars flowing through the world, the global economy is expanding, and it becomes more attractive and more widespread as an international liability currency. That’s when the transaction tickets are printed. The best times for Wall Street, The City and other metonyms for Metropolitan capital is when the dollar is weak, not when it is strong.

I have tried to suggest above how the narrative that dollar centrality is an exorbitant burden is mistaken. But this is not to say that I believe that the dollar centrality is an exorbitant privilege either. Other large developed countries with floating exchange rates manage to run large current account deficits, watch their currencies experience dramatic rises and falls, suffer occasional bouts of inflation or slowing and still fund themselves in global markets in their own currencies. So do an increasing number of top-tier emerging markets (though this is really more true for surplus East Asia, capital control-India, and Central and Eastern European members of the EU). I just don’t think it’s a very big deal. The dollar could become just another currency without great loss or gain for the US in economic terms, in my opinion.

Currency Roles as Fight Club

But that’s not true of power politics. The dollar’s centrality in the international monetary system as the universal fungible, asset, invoicing, and liability currency (I’m trying to launch UnFailing an acronym because I think it really captures its roles better than the partial “global reserve asset”) gives the US multiple arenas of suasion by curtailing not just the access to dollars, but even by curtailing access to the pipes through which the dollar flows. That is an enormously valuable tool that has been used repeatedly, and at ever greater scale. Threats to this role are taken seriously. The somewhat greater urgency at the Fed to consider a Central Bank Digital Currency seems driven in part by concern that fears that China will get there much faster. The worry is not that this would make the renminbi a full-scale competitor to the dollar, but that this could open transaction pipes that are transparent to China, but opaque to the US. Any attempts at the renminbiization of China’s BRI lending (which would make a lot of sense to from the point of view of China and its borrower countries that are exposed to the Chinese real cycle) might meet similar reservations.

Similarly, the ability of the US to rope European institutions into sanctions ventures where they were less enthusiastic (such as during the US withdrawal from the JCPOA under Donald Trump) was driven by need of European banks for dollar funding for their international business lines. One of the fundamental problems with the intermittent EU quest for strategic autonomy is that it has a banking system that is vastly more internationalized than its currency. And working on the frailties of the currency will take time, though I remain an optimist on that front. See here e.g., https://karthiksankaran.medium.com/how-i-learned-to-stop-worrying-and-mostly-love-the-euro-e87c3abc5445

But tradeoffs between economic costs and benefits of dollar centrality( which I think are not really that big either way, as noted above) and its big-stick geopolitical role also lead policy and opinion-makers to navigate the contradictions. That the fulcrum of US politics runs through the upper-midwest, and western Pennsylvania (areas where local economic troubles have been blamed on trade and the dollar ) even as the administration wields its tools of economic pressure on rivals and possibly wobbly allies will in my increase policy split personality on the global role of the dollar. Sometimes a Burden is more a Durden. And to my friends on the other side of this debate, I will say — please pick two circles, not three.